The Last-Mile Paradox: Unlocking Value Through Choice Architecture in Logistics

Executive Summary

The United Kingdom's e-commerce logistics sector stands at a critical inflection point, characterized by a deepening schism between operational volume and consumer satisfaction. As parcel volumes surge to record highs—surpassing 4.2 billion items in the 2024-25 period—the underlying infrastructure of the "last mile" is buckling under the weight of an obsolete, retailer-centric model that prioritizes cost over choice.

This research paper provides an exhaustive analysis of the structural failures plaguing the UK parcel delivery market, specifically the endemic lack of consumer agency at checkout. It evaluates the emerging business opportunities defined by the "carrier-agnostic" revolution and the critical role of technology middleware in bridging the gap between rigid logistics networks and fluid consumer expectations.

Our analysis identifies that the solution to the "Trust Deficit" in delivery is not merely operational refinement, but a fundamental decoupling of the purchase from the logistics provider. This requires a new layer of "Choice Architecture" a strategic combination of multi-carrier integration, dynamic logic, and user experience design to restore consumer sovereignty.

1. The Anatomy of Market Failure: A Crisis of Satisfaction

To understand the necessity for a radical shift in business models, one must first perform a forensic audit of the current market's performance. The data paints a picture of a sector that is statistically robust in volume but qualitatively fragile in consumer trust.

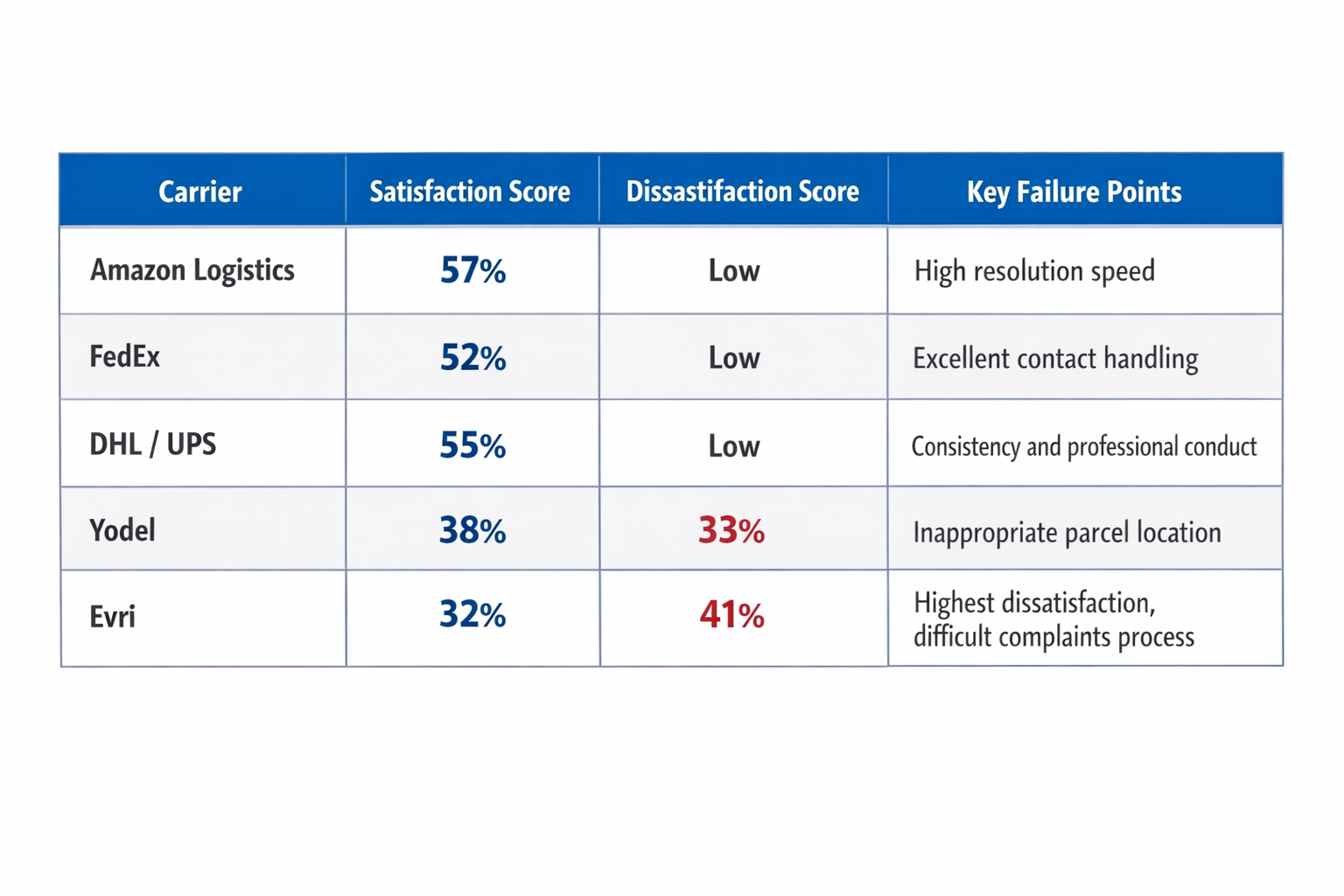

1.1 The Volume-Satisfaction Divergence

The UK parcel market is an engine of immense economic activity. According to Ofcom's Annual Monitoring Report on the Postal Market 2024-25, the sector processed a record 4.2 billion parcels, a 7% year-on-year increase that exceeds even the pandemic-induced peak of 2020/21. This volume growth indicates a permanent structural shift in British consumer behaviour, where e-commerce has transitioned from a convenience to a utility.

However, operational success masks a stagnation in service quality. While top-line satisfaction hovers around 78% , a deeper interrogation of the data reveals significant underperformance among the carriers handling the majority of non-Amazon volume. The "average" is buoyed by the exceptional performance of premium global integrators like FedEx, UPS, and DHL, which consistently score in the mid-to-high 50% range for customer satisfaction.

Beneath this tier lies the "volume/value" segment, dominated by carriers essential to the low-margin model of high-street fashion and general merchandise. These carriers consistently anchor the bottom of performance tables.

Table 1.1: Comparative Carrier Performance Metrics (2024-25)

Source: Ofcom Monitoring Reports 2024-25.

1.2 The Financial Impact of Failure on Retailers

The poor service levels described above are not just a consumer inconvenience; they act as a massive tax on the UK retail economy. The cost of "failed delivery" is a silent margin killer.

- Direct Costs: A single failed delivery costs a retailer approximately £11.60 in direct costs, including redelivery, customer service time, and potential refunds.

- Total Economic Impact: Failed deliveries drain an estimated £1.6 billion annually from UK retailers.

- Customer Churn: The "Trust Deficit" has long-term consequences. 70% of consumers are unlikely to return to a retailer after a poor delivery experience , and 43% of cart abandonments are attributed to a lack of preferred delivery options.

2. The Structural Root Cause: The "Black Box" Delivery Experience

If the cost of failure is so high, and consumer dissatisfaction so prevalent, why does the market not self-correct? Why do retailers continue to impose poor-performing carriers on their customers?

2.1 The Volume Discount Trap

Retailers are historically bound by the economics of volume. Logistics contracts are structured around tiered pricing. A retailer shipping 50,000 parcels a month negotiates a rate card with a single carrier to achieve the lowest possible unit cost. Splitting this volume across three carriers to offer consumer choice (e.g., Royal Mail, DPD, and Evri) would dilute their bargaining power, pushing them into more expensive pricing tiers.

2.2 Operational Rigidity

Physical fulfilment centres are optimized for flow and standardization. Managing multiple carriers requires segregating parcels into different cages, managing distinct label formats, and coordinating various collection times. Without sophisticated software, this "Operational Overhead" acts as a massive deterrent to multi-carrier adoption.

Consequently, the standard e-commerce experience in the UK remains a "Black Box." The consumer pays for the product and is assigned a carrier by the retailer's algorithm, usually based solely on the lowest cost, with no agency to signal their preference or veto carriers they distrust.

3. The Infrastructure Revolution: The Rise of the "Third Force"

While software solves the digital selection problem, physical infrastructure is required to execute the delivery. The most significant structural shift in the UK market is the emergence of a Carrier-Agnostic Infrastructure, spearheaded by the consolidation of InPost and Yodel.

3.1 The InPost/Yodel Hybrid Model

In early 2025, InPost acquired Yodel, one of the UK's largest courier firms. This acquisition, backed by private equity firm Advent International and PPF Group, fundamentally alters the UK logistics landscape.

- Strategic Rationale: The merger combines InPost's 18,000+ Out-of-Home (OOH) points (lockers and PUDO) with Yodel's door-to-door network handling 190 million parcels annually.

- The "Third Force": With a combined market share of approximately 8% and volumes exceeding 300 million parcels annually, this entity establishes itself as a genuine challenger to Royal Mail and Amazon.

3.2 The Shift to Out-of-Home (OOH)

The business case for this infrastructure is supported by shifting consumer behaviour.

- Generational Adoption: 66% of Gen Z shoppers have used parcel lockers in the last 12 months.

- Volume Surge: 115 million parcels were processed via UK lockers in the last year, driven by the convenience of 24/7 access and "label-free" returns.

4. The Business Opportunity: Choice Architecture

The convergence of high failure costs, new infrastructure, and consumer demand creates a specific market opportunity: The deployment of intelligent Choice Architecture.

4.1 The Role of Middleware

"Middleware" platforms such as Metapack, Sorted, and Sendcloud have emerged to abstract the complexity of carrier integration. By sitting between the retailer's Order Management System (OMS) and the carriers, these platforms allow retailers to access hundreds of services through a single API.

However, access to carriers is not enough. The competitive advantage lies in the logic of how these options are presented.

4.2 Dynamic Checkout and Conversion

Implementing "Dynamic Checkout" allows retailers to shift the cost decision to the consumer. Instead of a static £3.99 shipping fee, the software queries carrier APIs in real-time.

- The "Green" Nudge: Presenting a locker delivery as "0.8kg CO2" vs. home delivery as "2.5kg CO2" nudges consumers toward cheaper, sustainable options.

- The Reliability Premium: Data suggests 88% of consumers are willing to pay for faster, more reliable shipping. By offering a "Premium" slot powered by DPD alongside a "Standard" slot powered by Evri, retailers can monetize the demand for certainty.

5. Strategic Recommendations: The Role of the Integration Partner

The transition from a single-carrier model to a multi-carrier, consumer-centric model is not a plug-and-play exercise. It requires a fundamental re-engineering of the retailer's supply chain logic. This is where the concept of the "Choice Architecture" Consultant becomes critical.

5.1 The Complexity Gap

Retailers are often overwhelmed by the complexity of multi-carrier integration. While middleware providers sell the tool, they rarely provide the strategy. Retailers struggle with:

- Data Fragmentation: Integrating legacy ERPs with modern shipping APIs.

- Business Logic Configuration: Defining the complex rules that route heavy items to one carrier, high-value items to another, and remote postcodes to a third.

- UX Design: crafting a checkout interface that offers choice without causing decision paralysis.

5.2 The Need for Specialized Agencies

There is a distinct market for specialized partners who can bridge the gap between logistics operations and digital customer experience. These partners must:

- Audit the retailer's shipping profile to identify cost leaks and failure points.

- Implement the appropriate middleware (e.g., Sorted, Metapack, Fluent Commerce).

- Configure the "Business Logic"—the algorithmic rules that determine which carrier is displayed to the customer based on margin, weight, and destination.

- Design the checkout UX to maximize conversion, using behavioural nudges to guide customers toward the most efficient delivery methods.

6. Conclusion: Navigating the New Landscape with VE3

The problem of poor parcel delivery in the UK is a structural failure of market design. For too long, the "customer" of the carrier was viewed as the retailer, not the recipient. This alignment incentivized a race to the bottom on price, resulting in the fragile, low-trust ecosystem we see today.

The solution lies in restoring consumer sovereignty. Through the adoption of multi-carrier middleware and the transparency of dynamic checkout, the market can pivot. The "New Business Opportunity" is not just moving boxes; it is building the Choice Architecture that allows 67 million British consumers to decide exactly how, when, and where they receive their goods.

How VE3 Enable This Transformation

As a leader in digital transformation and supply chain optimization, VE3 is uniquely positioned to guide retailers through this complexity.

While software vendors provide the platform, VE3 provides the intelligence. Our approach combines deep expertise in:

- Supply Chain Digitization: We understand the operational realities of the warehouse and the data requirements of modern logistics.

- Customer Journey Mapping: We design checkout experiences that reduce abandonment and drive loyalty.

- Intelligent Integration: Leveraging our experience with cloud, data, and AI, we seamlessly integrate complex middleware into legacy retail stacks, ensuring that the "Business Logic" of delivery works for both the bottom line and the consumer.

By partnering with VE3, retailers can move beyond the "Black Box" of delivery, turning their logistics operations from a cost centre into a competitive advantage.

Visit us for more information or contact us directly.

.png)

.png)

.png)